Paper payment instruments remain relevant financial tools despite the widespread adoption of digital payment methods across modern banking systems today. Knowing how to write a check correctly prevents costly errors, protects against fraud, and ensures your payments reach intended recipients without complications or delays. Many people feel nervous completing these documents for the first time, worrying about making mistakes that might cause banking problems. This comprehensive guide walks you through every field, explains common mistakes, and builds the confidence you need to handle paper payments successfully.

Understanding Check Anatomy

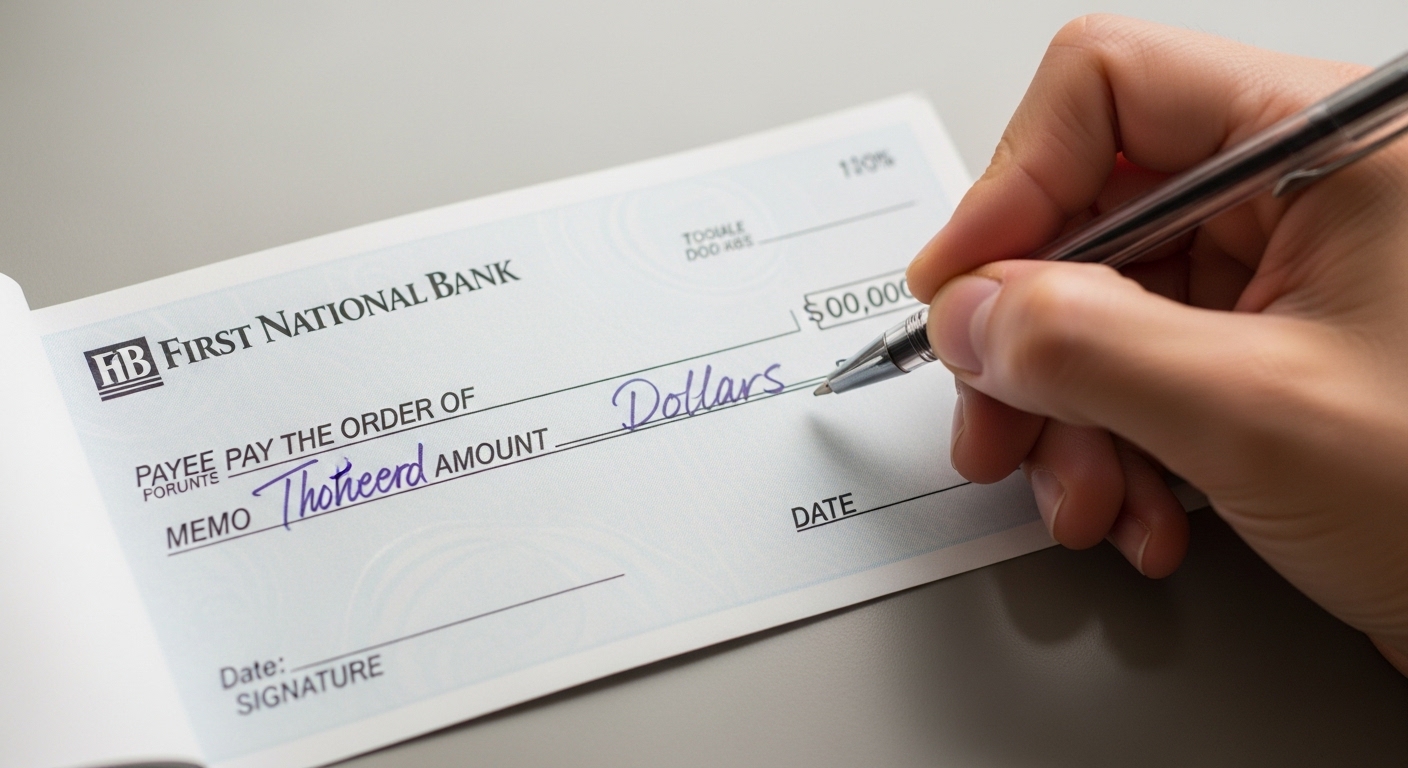

The Physical Layout

Before completing any payment document, you need to familiarize yourself with the different sections and fields that appear on its surface. Each area serves a specific purpose, and filling them out correctly ensures banks process your payment quickly and accurately without questions. Moreover, understanding the layout helps you avoid accidentally writing information in wrong spaces that create confusion for tellers and processors. Most standard personal documents share identical layouts regardless of which bank or financial institution prints and issues them to customers.

Preprinted Information

Banks preprint essential identifying information on each document before distributing them to account holders through mail or branch locations. Your name, address, bank name, routing number, and account number appear automatically on every document without requiring you to write them yourself. Additionally, each document carries a unique sequential number printed in the upper right corner that helps you track payments through your financial records. Furthermore, the routing number identifies your specific bank while the account number identifies your personal account within that institution’s system.

Security Features

Modern payment documents incorporate multiple security features that help banks detect alterations, counterfeiting, and fraudulent modification attempts during processing. Watermarks, security fibers embedded in paper, microprinting, and special inks make these documents difficult to reproduce or alter without obvious evidence appearing. Consequently, banks can verify authenticity during processing, protecting both you and the recipient from fraudulent substitution or alteration schemes. Additionally, using permanent ink pens provides your own security layer that prevents someone from erasing or chemically altering completed information after you write it.

Gathering Your Materials

Choosing the Right Pen

Always use a blue or black ballpoint pen with permanent ink that resists erasure and chemical alteration attempts by fraudsters. Gel pens sometimes bleed or smear in ways that obscure important information, so ballpoint options generally provide cleaner, more legible results. Moreover, never use pencils, felt-tip markers, or erasable pens that allow someone to modify completed payment documents after you’ve already signed them. Furthermore, pressing firmly enough to create clear impressions helps ensure that all information remains legible throughout the banking process.

Having Your Checkbook Ready

Keep your checkbook in a secure location and always have it accessible when you need to make payments requiring paper documents. Your checkbook register, the small booklet attached to your checks, helps you record each transaction and maintain accurate balance information. Additionally, recording transactions immediately after writing them prevents you from forgetting payments that might cause your balance calculations to become inaccurate. Consequently, maintaining your register diligently helps you avoid overdraft fees that occur when you spend more money than your account actually contains.

Verifying Account Information

Before writing a payment document for a large amount, verify that your account holds sufficient funds to cover the payment without triggering overdraft fees. Banks charge significant fees when payment documents bounce due to insufficient funds, and repeated occurrences can damage your banking relationship. Furthermore, some merchants and landlords charge their own returned payment fees on top of what your bank already charges for insufficient funds. Therefore, checking your balance through online banking, mobile apps, or ATM inquiries before writing large payments protects you from unnecessary and expensive financial penalties.

Step-by-Step Completion Process

Step One: Writing the Date

Locate the date line in the upper right corner of your document and write today’s complete date in the designated space. Most people write dates in month/day/year format such as February 17, 2026, though numerical formats like 02/17/2026 also work perfectly fine. Moreover, writing the correct current date helps you and your recipient track when the payment occurred for record-keeping and accounting purposes. Additionally, avoid post-dating documents by writing future dates, as banks can legally process them immediately regardless of what date you write on them.

Step Two: Filling the Pay To Line

The “Pay to the Order of” line requires the full legal name of the person or business you intend to pay with this document. Write the recipient’s name clearly and completely, using their official name exactly as it appears on their bank accounts or government identification. Furthermore, avoid abbreviations, nicknames, or informal versions of names that might cause problems when the recipient attempts to deposit or cash their payment. Additionally, leaving no space before the name and filling the entire line prevents someone from adding unauthorized names before or after what you’ve written.

Step Three: Writing the Numerical Amount

The small box on the right side of the pay line requires you to write the exact payment amount using numerals rather than words. Write the dollar amount clearly, starting as close to the left edge of the box as possible to prevent fraudulent number additions. Moreover, include cents after a decimal point even when paying exact dollar amounts, writing them as “.00” to show no additional cents apply. Furthermore, draw a line through any remaining empty space in the box after writing your amount to prevent unauthorized alterations to the numerical value.

Step Four: Writing the Written Amount

The long line below the pay-to line requires you to spell out the payment amount in words, beginning at the far left of the line. Write the dollar amount in words first, then express cents as a fraction over one hundred, such as “Twenty-five and 50/100.” Additionally, draw a straight line filling all remaining empty space on the line after your written amount to prevent unauthorized additions. Moreover, if the numerical and written amounts differ, banks typically honor the written amount, making accuracy in this field particularly critical for preventing payment errors.

Step Five: Completing the Memo Line

The memo line in the lower left corner provides optional space for noting the payment’s purpose or including relevant reference information for both parties. Writing an account number, invoice number, or brief description helps the recipient apply your payment to the correct account or invoice quickly. Furthermore, memo notes prove valuable when you review your own records months later and need to remember what specific payment covered or represented. Consequently, developing the habit of always completing the memo line creates more useful financial records without requiring significant additional time or effort.

Step Six: Signing Your Name

Your signature on the line in the lower right corner represents legal authorization for the bank to release funds from your account. Sign using the same signature you provided when opening your account, as banks compare signatures to verify authenticity during processing. Moreover, never sign documents before completing all other fields, as blank signed documents give anyone who finds them complete control over your bank account. Additionally, signing clearly and consistently helps bank employees verify authenticity quickly without requiring additional verification steps that delay payment processing.

Common Mistakes to Avoid

Leaving Blank Spaces

Empty spaces anywhere on completed payment documents create opportunities for dishonest individuals to add unauthorized information that increases payment amounts. Always fill remaining space on the amount line, pay-to line, and other fields with horizontal lines that prevent additions after completion. Furthermore, never hand someone a partially completed document and ask them to fill in missing information that you should complete yourself. Consequently, taking a few extra seconds to fill all spaces completely provides important protection against fraud that could cost you significant money.

Using Incorrect Recipient Names

Writing informal names, business nicknames, or incorrect legal names creates deposit problems when recipients attempt to process payments at their banks. Before writing a business name, verify the exact legal name they use for banking purposes, which sometimes differs from their commonly used trade name. Additionally, asking individuals for their full legal name rather than assuming you know the correct spelling prevents processing delays or outright rejection of your payment. Therefore, a quick phone call or email to verify the correct payee name saves both parties considerable inconvenience and frustration.

Mismatched Amounts

Writing different numbers in the numerical box versus the written line creates confusion that delays processing and may result in the wrong amount leaving your account. Always double-check that both representations match exactly before signing and releasing your completed payment document to the recipient. Furthermore, carefully verify that you’ve correctly moved decimal points, as accidentally writing one hundred dollars instead of ten dollars represents a significant error. Moreover, take your time completing amount fields rather than rushing, since errors in this area cause the most significant and difficult-to-resolve problems.

Forgetting to Record Transactions

Many people focus entirely on completing payment documents correctly but forget the equally important step of recording transactions in their checkbook register. Unrecorded payments create inaccurate balance information that leads to overdraft fees when you forget about outstanding payments during future spending decisions. Additionally, your bank statement shows processed payments but not those you’ve written that haven’t yet reached the bank for processing. Therefore, recording every transaction immediately after writing it maintains accurate running balances that prevent expensive overdraft situations and related banking complications.

Special Situations and Scenarios

Voiding a Check

Making an error while completing a payment document requires voiding it rather than attempting corrections that might create suspicious-looking alterations on the document. Write “VOID” in large, clear letters across the front of the document using permanent ink that cannot be removed or covered up effectively. Furthermore, record the voided document in your register with a note explaining why you voided it, which helps maintain accurate sequential records of all documents. Additionally, destroy voided documents by shredding them rather than simply throwing them away, as discarded banking documents create identity theft and fraud opportunities.

Providing Voided Checks for Direct Deposit

Employers and financial institutions frequently request voided documents to establish direct deposit or automatic payment arrangements that require your banking information. These voided documents provide routing and account numbers without authorizing any actual payment from your account for any purpose. Moreover, writing “VOID” clearly across the entire document prevents misuse while still providing all necessary banking information for legitimate setup purposes. Consequently, you can safely provide voided documents for these administrative purposes without worrying about unauthorized payment processing or account access.

Paying Cash at the Counter

Sometimes people make payment documents payable to “Cash” rather than a specific individual, creating a flexible document that anyone can cash. However, this practice carries significant risk because anyone finding a lost document made out to cash can immediately present it at any bank. Furthermore, making documents payable to cash undermines the security features that protect you when payments fall into wrong hands before reaching intended recipients. Therefore, always name a specific payee rather than using cash designations, regardless of the situation or the convenience this approach might seem to offer.

Writing Large Amount Checks

Particularly large payments deserve extra careful attention and verification before you complete and release them to ensure complete accuracy. Consider calling your bank before writing very large amounts to verify your balance and alert them to the upcoming large transaction. Additionally, some banks place temporary holds on large deposits, which might affect when the recipient gains access to funds from your large payment. Furthermore, keeping copies of large payment documents and noting all relevant details creates important records for your personal financial documentation and potential future reference needs.

Security Best Practices

Protecting Your Checkbook

Store your checkbook in a secure location at home and avoid carrying your entire checkbook when you only need one or two documents. A stolen checkbook gives thieves access to multiple blank documents that they could use to drain your bank account completely. Moreover, report a lost or stolen checkbook to your bank immediately so they can flag your account and watch for suspicious activity. Additionally, consider ordering smaller quantities of documents at a time to limit your exposure if they become lost or stolen before you use them.

Monitoring Your Account

Review your bank statements carefully each month, comparing each processed payment against your personal register entries to identify discrepancies quickly. Online banking makes daily balance monitoring easy and allows you to catch unauthorized transactions before they multiply or compound into larger losses. Furthermore, many banks offer text or email alerts that notify you whenever your account processes a payment, providing real-time fraud detection capabilities. Consequently, prompt attention to account monitoring catches problems early when banks can still reverse unauthorized transactions and help you recover funds.

Ordering Replacement Checks Safely

Always order replacement documents directly through your bank or a reputable printing company rather than using unknown or suspicious third-party services. Some fraudulent companies collect banking information from people ordering documents and use it for identity theft or unauthorized account access. Additionally, verify that replacement documents arrive in tamper-evident packaging and report missing shipments to your bank immediately if deliveries don’t arrive as expected. Moreover, shred any promotional materials offering discount document printing that arrive unsolicited, as these sometimes represent data collection schemes targeting banking customers.

Transitioning to Digital Alternatives

When Paper Payments Still Make Sense

Despite the availability of digital payment options, certain situations still favor traditional paper payment methods for various practical reasons. Some small businesses, individual contractors, and landlords prefer paper payments because they avoid credit card processing fees that reduce their income. Additionally, certain formal payments like security deposits, legal settlements, and government fees sometimes require traditional payment methods by policy or regulation. Furthermore, older recipients who lack digital banking comfort or reliable internet access genuinely benefit from payment methods that don’t require technological sophistication or connectivity.

Comparing Payment Methods

Electronic transfers, online bill payments, and digital wallets each offer convenience advantages that paper payments cannot match in modern financial environments. However, paper payments provide a physical paper trail that some people find reassuring for their personal record-keeping and dispute resolution needs. Moreover, digital payments fail when systems experience outages, while paper payments provide a reliable backup option that functions independently of technology infrastructure. Consequently, maintaining familiarity with both traditional and digital payment methods gives you maximum flexibility to choose the most appropriate option for each situation.

Mobile Deposit Considerations

Many banks now accept photographs of paper documents through mobile banking applications, making remote deposit without visiting physical branches possible. Recipients can deposit received payments by photographing both sides of their document using their bank’s mobile application quickly and conveniently. Furthermore, this technology makes paper payments more convenient for recipients while allowing payers to continue using familiar traditional methods they prefer and trust. However, recipients should follow their bank’s instructions about retaining original documents after mobile deposit in case verification becomes necessary later.

Teaching Check Writing to Others

Helping Teenagers Learn

Young adults entering financial independence benefit enormously from learning paper payment skills before they encounter situations requiring them unexpectedly. Parents should walk teenagers through actual practice examples using voided or practice documents before requiring them to complete real payments independently. Additionally, explaining why each field exists and what problems arise from errors helps young people understand the importance of careful attention to detail. Consequently, young adults who receive this guidance approach financial responsibilities more confidently than peers who never received practical payment education.

Supporting Elderly Family Members

Some older adults who have written payments for decades may develop difficulties with handwriting legibility or remembering all required steps due to age-related changes. Family members can support aging relatives by reviewing completed documents before mailing them, helping catch errors before they create problems. Furthermore, larger-print checkbook registers and writing guides that align over documents help people with vision challenges maintain independence in managing their finances. Moreover, patient, respectful guidance helps elderly family members maintain financial independence and dignity longer than they might otherwise manage alone.

Keeping Good Records

Checkbook Register Management

Your register represents a complete running record of every transaction affecting your account, making regular maintenance absolutely essential for financial accuracy. Record each payment immediately after completing it, including the document number, date, recipient name, amount, and purpose in appropriate columns. Additionally, subtract each payment from your running balance immediately so you always know exactly how much money your account currently contains. Furthermore, compare your register balance against your bank statement monthly to catch discrepancies that might indicate errors, missed recordings, or fraudulent activity.

Digital Record Keeping

Photographing completed documents before releasing them creates digital backup records that you can access easily if disputes or questions arise later. Cloud storage services allow you to organize these photographs by date and recipient, creating searchable digital archives of your complete payment history. Moreover, digital records survive house fires, floods, and other disasters that might destroy paper records you’ve carefully maintained in physical files. Consequently, combining traditional paper register entries with digital photograph backups creates redundant record systems that protect your financial documentation comprehensively against various loss scenarios.

Conclusion

Mastering paper payment completion remains a valuable financial skill despite the growing dominance of digital alternatives in contemporary banking environments. Each field on these documents serves a specific protective or informational purpose that contributes to secure, accurate payment processing for all parties involved. Moreover, understanding common mistakes and how to avoid them prevents costly errors, bounced payments, and potential fraud vulnerability from careless completion habits. By following the step-by-step guidance in this article, you can complete payment documents confidently and correctly every single time. Additionally, combining careful completion habits with diligent record keeping and account monitoring creates comprehensive financial management practices that serve you well throughout your entire financial life.